You are on our wealth management services website for advisors & wealth managers.

Browse more Fidelity websites here.

Year after year, you and your child have been saving for college through a 529 savings account. Now college is closer and it's time to think about spending the money you've put aside. You'll be in control of how much is withdrawn and how it'll be used, but there are a few things you need to know up front to make the most of your savings.

First, a reminder about federal gift tax limits: In 2026, you can gift up to $19,000 per parent in a 529 account, or $38,000 per couple. Grandparents can also contribute up to $38,000 as a couple per beneficiary per year. Contributing more than $19,000 per beneficiary would need to be reported to the IRS as a gift. However, with "accelerated gifting,"1 a 529 account can be funded with contributions of $95,000 per person or $190,000 per couple—which uses up your federal gift-tax exclusion for 5 years.

What can you use this money for? Which expenses trigger taxes and penalties? If you do things right, no penalties or federal income tax—and, in many states, no state income tax—will be due on your withdrawals. But learning by trial and error can be costly at tax time, and more importantly, your child could lose out on financial aid if you're not careful. So learn the ins and outs ahead of time.

Here's a 9-step guide to help you make your 529 savings go as far as possible.

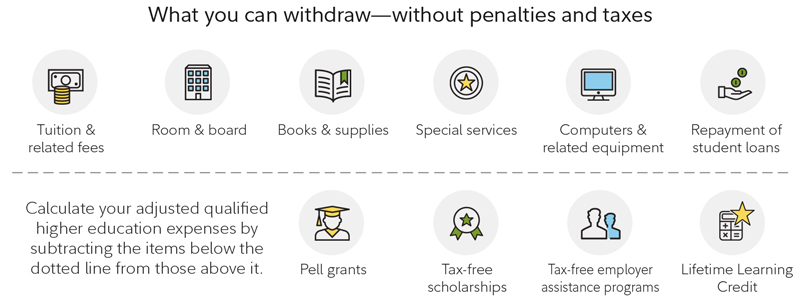

Qualified withdrawals are federal income tax-free so long as the total withdrawals for the year don't exceed your child's adjusted qualified higher education expenses (QHEEs), discussed in #3 below.

To calculate these, add up tuition and fees, room and board, books and supplies, any school-related special services, and computer costs, and then deduct any costs already covered by tax-free educational assistance. Examples include Pell grants, tax-free scholarships and fellowships, tuition discounts, the Veteran's Educational Assistance Program, and tax-free employer educational assistance programs.

But you're not done yet. You'll also need to deduct costs used to claim an American Opportunity Tax Credit or Lifetime Learning Credit. The basic rule: You can't double up tax benefits for the same college expenses, discussed in #5.

For full details, see footnote3

Money saved in a 529 plan can also be used to pay qualified expenses associated with college or other postsecondary training institutions. Eligible schools include any college, university, vocational school, or other postsecondary educational institution eligible to participate in a student aid program administered by the U.S. Department of Education. When you pay qualified education expenses from a 529 account, your withdrawals are federal-income-tax- and penalty-free.

While funds from a 529 account can be used to pay for expenses required for college, not all expenses qualify. Tuition and fees are considered required expenses and are allowed, but when it comes to room and board, the costs can't exceed the greater of the following 2 amounts:

In other words, if your child is planning to live off campus in housing not owned or operated by the college, you can't claim expenses in excess of the school's estimates for room and board for attendance there. So it's important to confirm room and board costs with the school's financial aid office in advance so you know what to expect. Also, keep in mind that in order for room and board to qualify, your child must be enrolled half time or more.

Note, too, that as of 2019, "qualified expenses" include tuition expenses for elementary, middle, and high schools (private, public, or religious). Although the money may come from multiple 529 accounts, only $20,000 total can be spent each year per beneficiary on elementary, middle, or high school tuition and other qualified expenses.

Textbooks count as an education expense, but only those included on the required reading for the course.

Computers and related equipment and services are considered qualified expenses if they are used primarily by the beneficiary during any of the years that the beneficiary is enrolled at an eligible educational institution. Computer software for sports, games, or hobbies would be excluded unless the software is predominantly educational in nature.

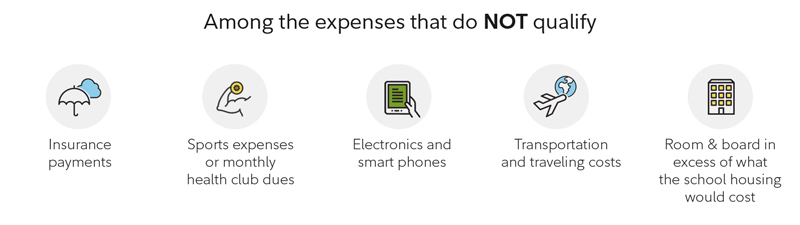

It's important to make sure that items purchased are qualified expenses and to keep receipts of purchase. Be careful to avoid expenses that don't qualify—for example, equipment used primarily for amusement or entertainment doesn't qualify. These and other lifestyle expenses, like insurance, sports expenses, health club dues, and travel and transportation costs, will have to be funded through other resources. If you're not sure whether a plan covers a particular college expense, the college's financial aid office should be able to help.

Check with the school to find out exactly what's required so you can avoid accidentally taking a nonqualified distribution. If you withdraw money for anything that doesn't meet the qualified expense criteria, any part of the distribution that is made up of earnings on contributions will be taxed as ordinary income and could incur a 10% federal penalty. However, the penalty may be waived if there are extenuating circumstances, such as the disability or death of the beneficiary, or if the beneficiary receives a scholarship, or attends a US military academy.

Your 529 savings plan administrator will, in most cases, provide an annual statement that reports your contributions and earnings, including the amount you withdrew from the plan. But it's you, not your program provider, who is responsible for accurately reporting to the IRS. If your withdrawals are equal to or less than your qualified higher education expenses (QHEEs), then your withdrawals including all your earnings are tax-free. If your withdrawals are higher than your QHEE, then taxes, and potentially a penalty, will be due on earnings that exceed your qualified expenses. For many people, keeping track is easy because large tuition bills use up most of their 529 savings. But if you are using your 529 plan for room and board expenses, it's smart to keep those receipts.

It's important that withdrawals you take from your 529 savings account match the payment of qualifying expenses in the same tax year. Like some families, you may choose to pay the school directly from your 529 account for ease in recordkeeping and matching distributions to school expenses. In this situation, make sure you are aware of school payment deadlines and the time required to transfer funds from the 529 account to the school. It can take several days for investments to be sold out of your 529 account and mailed to the school and then a week or so for the payment to make it through the mail and then processed by the school.

Or you may choose to move money from your 529 account to your bank or brokerage account. Many colleges prefer payments to be made electronically through their website from a bank or brokerage account. You can choose to pay bills first and then reimburse yourself from the 529 account, or you can pull money from the 529 account and then use it to pay bills from your bank or brokerage account. This path also provides flexibility when paying smaller bills like those for books or off-campus room and board.

Keep in mind that you must submit your request for the cash within the same calendar year—not the same academic year—as you make the payment. If the timing is off, you risk owing tax because it's considered a non-qualified withdrawal.

If you're enrolled in a plan through a financial professional, contact them when you're ready to withdraw funds. If you have a direct 529 plan, contact the plan administrator for withdrawals. Remember to build in time for processing.

Another withdrawal option: You could have the money distributed from the 529 account to your child. If some of the money is used for non-qualified expenses, such as buying a car, there may be reportable earnings—which will go on your child's tax return—and a 10% penalty would apply. Any earnings are taxed at your child's lower tax bracket—unless the so-called "kiddie tax" applies. The kiddie tax requires certain children as old as 23 to pay tax on unearned income at their parents' marginal tax rate. Check with your tax professional to see if this applies and how this option would impact student aid eligibility.

If you are interested in distributing money directly to the beneficiary, ask your plan provider for instructions.

Another reason to have the distribution sent to your child is that it may be possible to wipe out any resulting tax with an American Opportunity Tax Credit or Lifetime Learning Credit, as explained in #5. Because of income limitations, you may not be eligible to claim these credits on your own return. Remember though, if the payments are used for a qualified higher education expense, no federal taxes are owed.

Ask your plan provider for instructions if you are interested in distributing money directly to the beneficiary.

The federal government offers additional tax incentives to help ease the burden of some college expenses, but unfortunately, you won't be able to use a 529 account to cover those same expenses. If you do, the IRS will consider it double dipping, so you'll want to factor in whether you'll be claiming this tax credit when deciding how much to withdraw from your 529 account. These tax credits may also affect your child's eligibility for financial aid.

Below are the 2 most common tax credits. Remember, a credit goes directly against your tax liability, which is different from a deduction. Only one credit can be claimed for a student each year.

If your child has more than one 529 savings account, such as an additional account through a grandparent, knowing which account to use first or how to take advantage of them concurrently could help. Don't leave decisions to the last minute—instead, sit down with all plan owners and decide on a withdrawal strategy ahead of time to make sure the qualifying college costs are divvied up in the most beneficial way.

With careful planning, you can avoid having money left over in your 529 account once your child graduates. But if funds remain, there are several options available. You can let the money sit in the account in anticipation of your child continuing on to graduate school or another post-secondary institution. If so, you'll want to rethink your investment strategy depending on how soon the funds will be needed so you can take full advantage of the potential for growth over time.

If your child does not have any more college costs, you have other options to use the funds without occurring a tax or penalty:

Regardless of which option you choose, you may want to rethink your investment strategy, depending on how soon the funds will be needed.

Also, each state has different restrictions on 529 accounts, so check with your financial advisor or ask your plan provider for the specific requirements of your plan.

Note, too, that The SECURE 2.0 Act allows, with restrictions, leftover 529 funds to be rolled over into a Roth IRA4. Please consult a financial or tax professional regarding your specific circumstances before making any investment decision.

What if the beneficiary gets a scholarship? You'll be happy to learn that there is a scholarship exception to the 10% penalty. You can take a non-qualified withdrawal from a 529 account up to the amount of a scholarship; although you will pay taxes on the earnings, you won't pay the additional 10% penalty that's imposed on a non-qualified withdrawal. Remember to ask for a scholarship receipt for your tax records.

If you'll count on financial aid to supplement your college savings, you'll want to do what you can to improve your eligibility. While individual colleges may treat assets held in a 529 plan differently, in general these assets have a relatively small effect on federal financial aid eligibility. Because 529 plan assets are considered assets of the parent, they tend to have a small effect when the government calculates your financial aid eligibility, whereas accounts that are considered assets of the child, such as an UGMA or UTMA account, tend to have a greater effect on federal financial aid eligibility. (Note that 529 accounts owned by grandparents are not included in the student aid index calculation.)

If you're thinking of taking out loans that start incurring interest immediately, you may want to spend 529 funds first, deferring these loans until later. Another situation that would call for using 529 plan funds first would be if there's a chance your child may graduate earlier or receive some other funding down the road, such as a scholarship.

At some point, you'll actually need to start spending the money you've set aside. You will need to think about preserving gains you may have made so that funds will be there when they're needed. If your plan relies on an age-based investment strategy, this process is already in place and your asset mix has slowly evolved toward more conservative investments like money market funds and short-term bonds.

Now's the time to sit down with all the contributing family members and your child and create a withdrawal plan that's ready to set in motion. It's a smart idea to spend from the plan in established increments, and withdraw wisely from your college savings plans, so you can reap the tax advantages and avoid mistakes along the way.

Manage client portfolios with greater efficiency and impact with our broad universe of portfolio construction solutions and investment products.

Learn more

Find out how our team can support you and your firm with data-rich and personalized content designed to help you optimize client outcomes and drive sustainable growth.

Learn more

Explore the exciting world of digital assets, with a focus on blockchain technology, cryptocurrency investing, and more.

Learn more

1. Accelerated gifting, or an accelerated transfer, to a 529 plan (for a given beneficiary) of $95,000 (or $190,000 combined for spouses who gift split) will not result in federal transfer tax or use of any portion of the applicable federal transfer tax exemption and/or credit amounts if no further annual exclusion gifts and/or generation-skipping transfers to the same beneficiary are made over the 5-year period and if the transfer is reported as a series of 5 equal annual transfers on Form 709, United States Gift (and Generation-Skipping Transfer) Tax Return. If the donor dies within the 5-year period, a portion of the transferred amount will be included in the donor's estate for estate tax purposes.

2.529 distributions for qualified education expenses are generally federal income tax free. 529 assets may be used to pay for (i) qualified higher education expenses, (ii) qualified expenses for registered apprenticeship programs, (iii) up to $20,000 per taxable year per beneficiary for tuition expenses in connection with enrollment at a public, private, and religious elementary and secondary educational institution. Although such assets may come from multiple 529 accounts, the $20,000 qualified withdrawal limit will be aggregated on a per beneficiary basis. The IRS has not provided guidance to date on the methodology of allocating the $20,000 annual maximum among withdrawals from different 529 accounts, (iv) amounts paid as principal or interest on any qualified education loan of a 529 plan designated beneficiary or a sibling of the designated beneficiary. The amount treated as a qualified expense is subject to a lifetime limit of $10,000 per individual. Although the assets may come from multiple 529 accounts, the $10,000 withdrawal limit for qualified educational loans payments will be aggregated on a per individual basis. The IRS has not provided guidance to date on the methodology of allocating the $10,000 annual maximum among withdrawals from different 529 accounts, and (v) tuition, fees, books, supplies, and equipment required for the enrollment or attendance in a recognized postsecondary credential program as defined under Section 529 of the Code and identified by the Secretary of the Treasury as being such a reputable program.

Any earnings on distributions not used for qualified higher educational expenses or that exceed distribution limits may be taxed as ordinary income and may be subject to a 10% federal tax penalty. Some states do not conform with federal tax law. Please check with your home state to determine if it recognizes the expanded 529 benefits afforded under federal tax law, including distributions for elementary and secondary education expenses, apprenticeship programs, postsecondary credentialing programs, and student loan repayments. You may want to consult with a tax professional before investing or making distributions.

K-12 qualified expenses in addition to tuition include: Curriculum and curricular materials, books or other instructional materials, online educational materials, tuition for tutoring or classes outside of the home (if the tutor is not related to the student, is licensed as a teacher in any state or has taught at an eligible educational institution or is a subject matter expert in the relevant subject), fees for a nationally standardized achievement test, advanced placement exam, or college admission exam, fees for dual enrollment in an institution of higher education, and educational therapies for students with disabilities provided by a licensed provider, including occupational, behavioral, physical, and speech-language therapies. Fidelity does not provide legal or tax advice. The information herein is general and educational in nature and should not be considered legal or tax advice. Tax laws and regulations are complex and subject to change, which can materially impact investment results. Fidelity cannot guarantee that the information herein is accurate, complete, or timely. Fidelity makes no warranties with regard to such information or results obtained by its use, and disclaims any liability arising out of your use of, or any tax position taken in reliance on, such information. Consult an attorney or tax professional regarding your specific situation.

3. Savingforcollege.com, Avoid these 529 withdrawal traps.

4. Beginning January 2024, the Secure 2.0 Act of 2022 (the "Act") provides that you may transfer assets from your 529 account to a Roth IRA established for the Designated Beneficiary of a 529 account under the following conditions: (i) the 529 account must be maintained for the Designated Beneficiary for at least 15 years, (ii) the transfer amount must come from contributions made to the 529 account at least five years prior to the 529-to-Roth IRA transfer date, (iii) the Roth IRA must be established in the name of the Designated Beneficiary of the 529 account, (iv) the amount transferred to a Roth IRA is limited to the annual Roth IRA contribution limit, and (v) the aggregate amount transferred from a 529 account to a Roth IRA may not exceed $35,000 per individual. It is your responsibility to maintain adequate records and documentation on your accounts to ensure you comply with the 529-to-Roth IRA transfer requirements set forth in the Internal Revenue Code. The Internal Revenue Service (“IRS”) has not issued guidance on the 529-to-Roth IRA transfer provision in the Act but is anticipated to do so in the future. Based on forthcoming guidance, it may be necessary to change or modify some 529-to-Roth IRA transfer requirements. Please consult a financial or tax professional regarding your specific circumstances before making any investment decision.