You are on our wealth management services website for advisors & wealth managers.

Browse more Fidelity websites here.

Mounting worries about ballooning US deficits have roiled the bond market, sending long-term bond rates to new highs, despite the Fed’s recent cuts in short-term rates. Does that mean investors should be wary of Treasury and other high-quality bonds now?

That could be a mistake, says Robin Foley, Head of Fixed Income at Fidelity. "I believe it to be a good time for bonds, even if some people don't think so," she says.

To be sure, risks exist in bonds, just as they do in any investment. Fidelity's Asset Allocation Research Team agrees that rising government debt has long-term implications for both stock and bond markets. However, there are plenty of reasons to believe that bonds can continue to play a useful role in diversified portfolios in the second half of 2025 and beyond.

If an investor is looking for income from individual bonds, current yields near multi-decade highs in longer-term bonds can offer an opportunity. And if they are considering bond funds or ETFs to diversify their portfolio, Fidelity's bond managers believe that a combination of high current yields and interest rates that are expected to gradually fall later this year is creating an attractive total return opportunity for bond investors in the months ahead.

Michael Plage, a portfolio manager at Fidelity, believes that the second half of 2025 is likely to be a good time for skilled bond investors to take advantage of that potential opportunity.

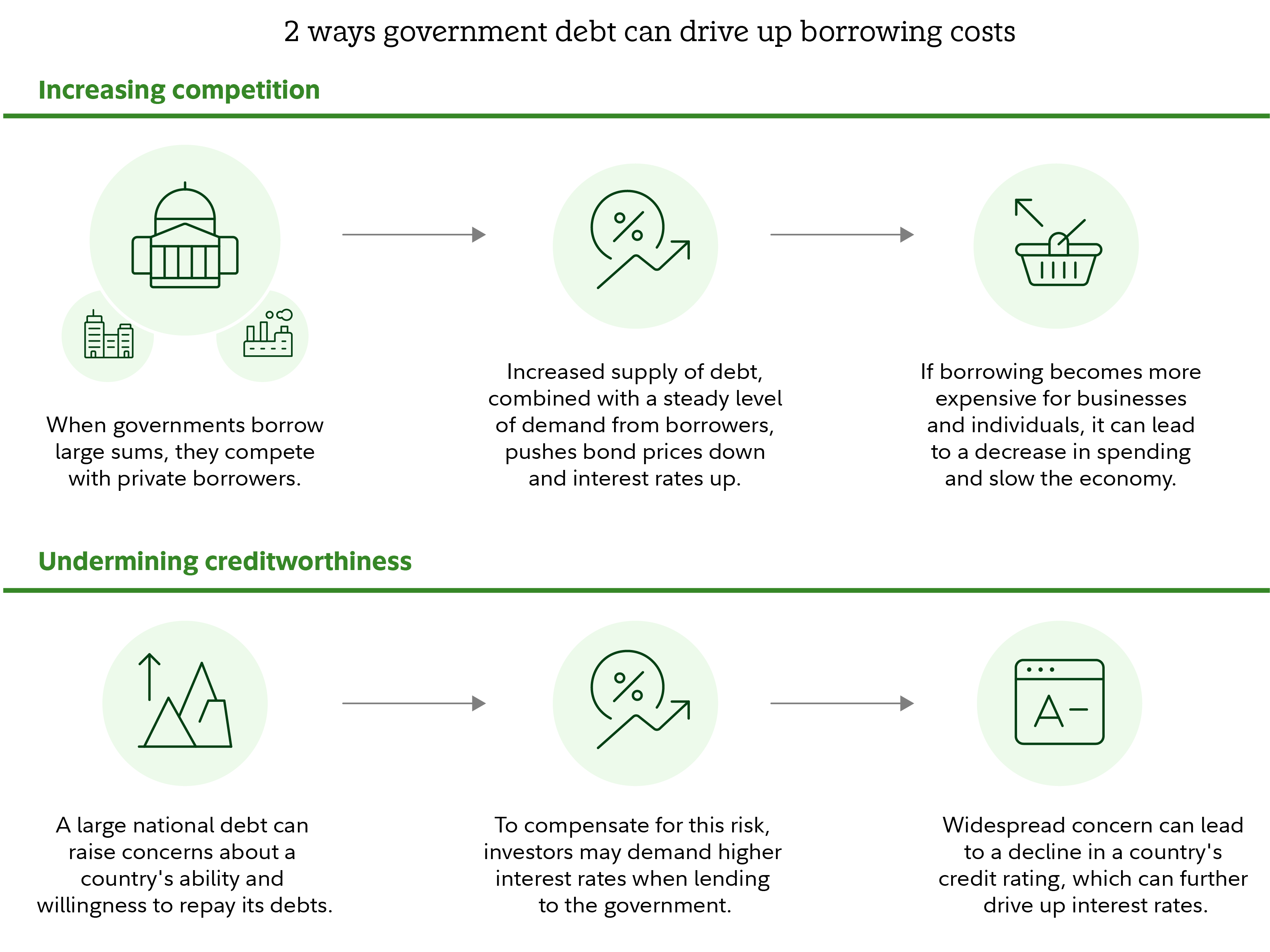

The US and most developed market economies have high levels of government debt and some long-term investors have begun to demand higher yields in return for loaning money to these governments for 10 years or longer. Their concern is that higher debt and resulting long-term inflation will reduce the value of the fixed interest payments they receive on those bonds. In response, they have begun to demand what is called a term premium, which is a higher yield on longer-term bonds.

Despite the newfound concern being expressed about the threat of rising debt to bond markets, high government debt is not new, unique to the US, or only a risk to bonds. The surge in concern about how it might eventually affect bonds should not obscure other factors which may matter more for bond investors in the nearer term. These include attractive yields and the likelihood that interest rates will move lower, both of which may give high-quality, low-risk investment-grade bonds the potential to deliver both attractive interest payments and more potential for capital appreciation than stocks or cash in the months ahead.

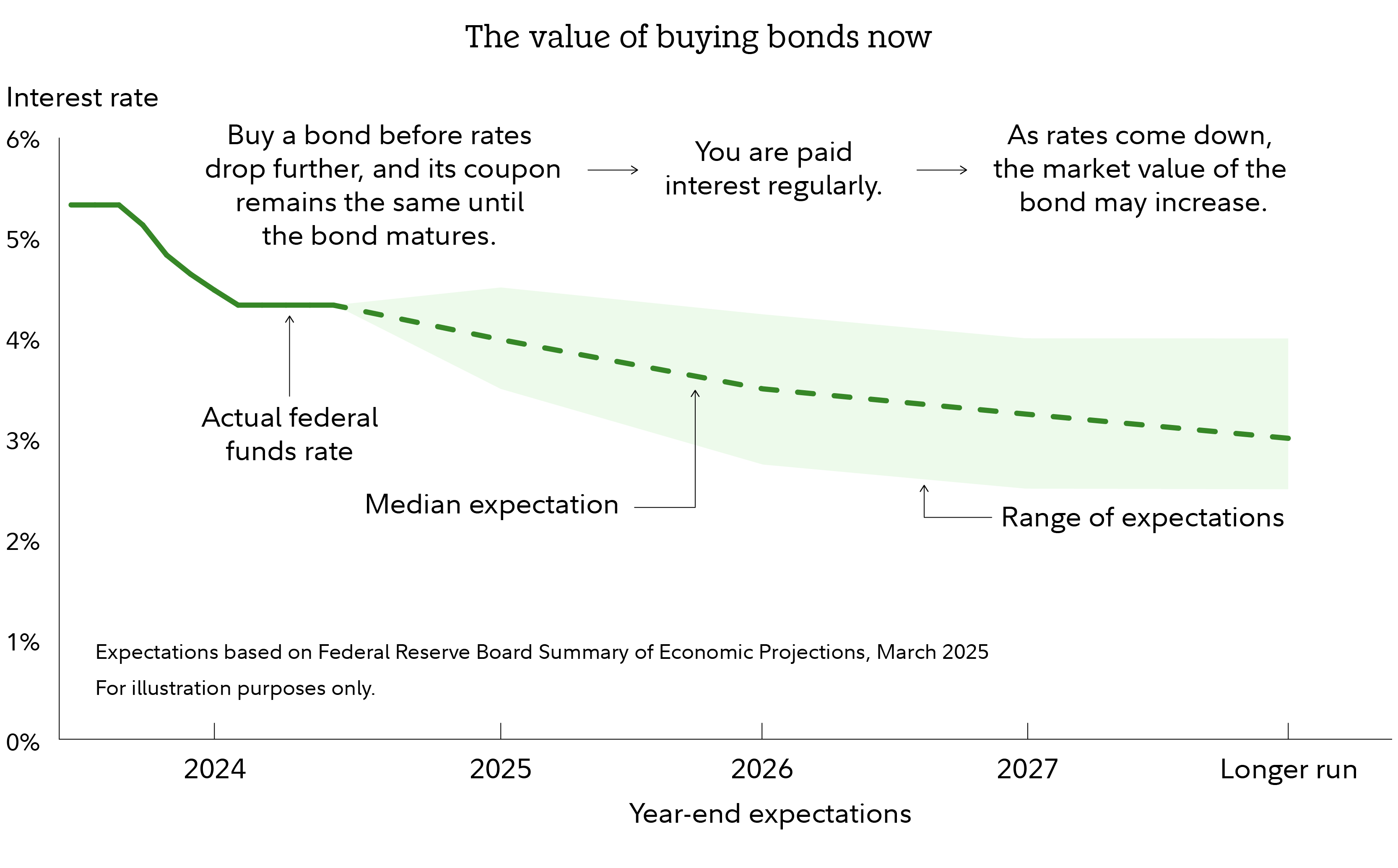

To understand why opportunity exists in bonds in the second half of 2025, it’s important to remember where bond returns come from. A bond can deliver return to its owner from 2 sources: interest payments known as coupons whose rate is set at the time the bond is issued, and changes in the price of the bond as it trades in the market.

The interest rate of the coupon remains the same until the bond matures but the price can rise or fall throughout the trading day. Because bond prices typically rise when interest rates fall, the best way to earn a high total return from a bond or bond fund is to buy it when interest rates are high but coming down. Past performance is no guarantee of future results, but in similar periods historically, investors have been able to lock in still relatively high coupon yields and also enjoy the increase in the market value of their bonds as rates come down and prices rise.

Plage believes that bonds in the second half of 2025 present a unique and appealing opportunity for investors who have been sitting in money market funds or short-term CDs to not only lock in longer-term coupon income and seek potential capital appreciation, but also to reduce risk in their portfolios. Yields on CDs and money markets rose to roughly 5% after the Fed began raising short-term interest rates in 2022. But those yields have moved lower following a series of Fed rate cuts late last year and are widely expected to fall further and stay lower than they had been. That raises the risk that investors who need a certain level of income from their portfolios won’t get it if they stay in cash or short-term investments like money market funds and short-term CDs.

The return of a term premium to longer-maturity bonds has been one of the more significant forces driving bond markets so far in 2025 and it's likely to remain so through the second half of the year. While the revival of demand by investors for higher long-term yields has helped fuel volatility so far this year, it may also be a sign that the bond market is returning to how it has behaved throughout most of history, where supply and demand, rather than central bank monetary policy, drive the market.

Since the financial crisis, bond yields have been strongly influenced by the policy of the Federal Reserve, which has kept rates low and liquidity abundant through its policy of buying large quantities of US Treasury bonds. As the Fed has stepped back from this policy known as quantitative easing though, market forces that used to play a greater role in determining bond yields and prices are beginning to do so again. The most notable example of this is currently in long maturity US Treasury bonds. While the return of the term premium after its long QE-induced nap has been startling so far this year, the return of a more historically normal bond market may be creating opportunity for some investors in individual longer-term bonds.

Whether the rising term premium is an opportunity or a risk may depend on the amount of money an investor has to invest, their needs for income, and their time horizon. If an investor has several hundred thousand dollars to invest and can hold their bonds to maturity, they may be able to construct a portfolio of high-quality, low-risk bonds with reliable yields that are higher than other fixed income or short-term cash investments.

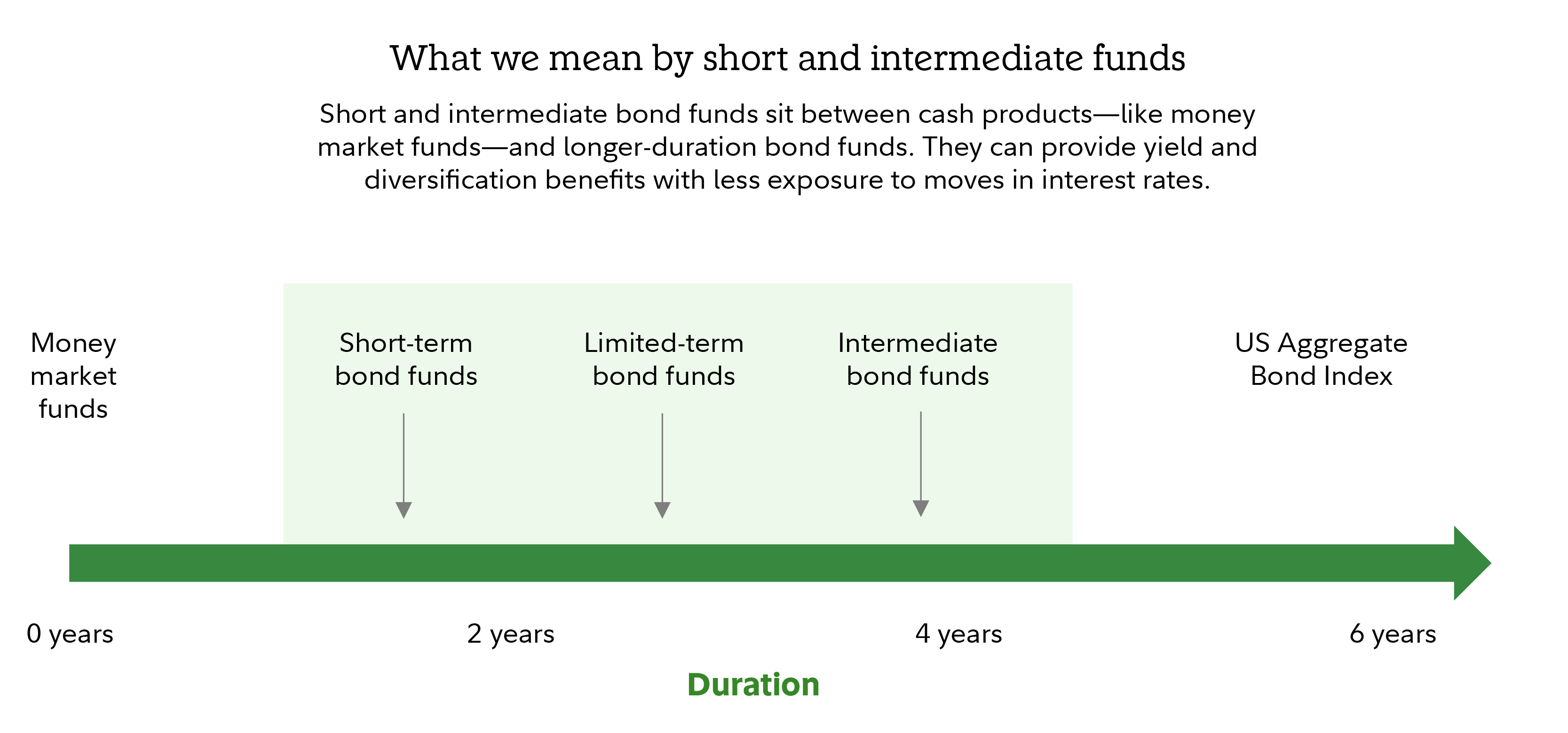

If an investor wants to invest in bond funds instead of individual bonds, the rising term premium on longer-maturity bonds may mean increased price volatility (which they may not want from their bond portfolio) in bond funds. One way to potentially reduce this risk is by investing in bond funds that own short and intermediate investment-grade debt.

“Short and intermediate bond funds might offer their most compelling storyline since 2008—a potential return advantage, relatively low volatility, and some of the highest starting yields in years,” says Michael Scarsciotti, head of the investment specialists at Fidelity Investments. While past performance is no guarantee of future returns, since 2012, these funds, on average, have generated 88% of the return of longer-term core bonds with 52% less volatility. That’s because shorter-term bonds have shown less sensitivity over time to changes in interest rates.

In the second half of 2025, Fidelity bond managers are also keeping an eye on the relationship between stock prices and bond prices. Bonds and stocks have historically moved in opposite directions, which has meant that bonds have been able to preserve the value of investors' portfolios when stocks have fallen. So far in 2025, bond and stock prices have been more correlated than they have been historically. Institutional Portfolio Manager Beau Coash believes that relationship may normalize in the months ahead as well. “I still believe bonds can help provide portfolio stability and may help mitigate risks during extreme stock market downturns,” he says. "Some investors may look at the recent correlation with stocks and the unexpected Treasury moves and decide that bonds aren’t a reliable source of ballast for their portfolios. But over longer time frames, I’ve noted low correlations between bonds and stocks.”

Buying shares of a bond mutual fund or ETF is an easy way to add a bond position. Bond funds hold a wide range of individual bonds, which makes them an efficient way to diversify your holdings even with a small investment.

An actively managed fund also gives you the benefits of professional research. For example, the managers can make decisions about which bonds to buy and sell based on huge volumes of information including bond prices, the credit quality of the companies and governments that issue them, how sensitive they may be to changes in interest rates, and how much interest they pay.

Not all bond funds are actively managed. Investors who seek bond exposure in a fund can also choose among exchange-traded and index funds that seek to track bond market indexes such as the Bloomberg US Aggregate Bond Index.

Here's more about the difference between investing in bond mutual funds or ETFs and individual bonds.

If an investor has enough money and believes they have the time, skill, and will to build and manage their own portfolio, buying individual bonds may be appealing. Unlike investing in a fund, doing it themselves lets an investor choose specific bonds and hold them until they mature, if they choose. However, an investor still would face the risks that an issuer might default or call the bonds prior to maturity. This approach requires an investor to closely monitor the finances of each issuer whose bonds they're considering. An investor also needs enough money to buy a variety of bonds to help diversify away at least some risk. If an investor is buying individual bonds, Fidelity suggests they consider spreading investment dollars across multiple bond issuers.

Fidelity offers over 100,000 bonds, including US Treasury, corporate, and municipal bonds. Most have mid- to high-quality credit ratings that would be appropriate for a core bond portfolio.

Separately managed accounts (SMAs) combine the professional management of a mutual fund with some of the customization opportunities of an investor doing it themselves. In an SMA, an investor invests directly in the individual bonds, but they are managed by professionals who make decisions based on factors such as current market conditions, interest rates, and the financial circumstances of bond issuers.

Whatever an investor's bond investing goals may be, professionally managed mutual funds, active ETFs, or separately managed accounts can help.

Access economic, fundamental, and quantitative analysis from our Asset Allocation Research Team.

Learn more

Manage client portfolios with greater efficiency and impact with our broad universe of portfolio construction solutions and investment products.

Learn more

Before investing in any mutual fund or exchange-traded fund, you should consider its investment objectives, risks, charges, and expenses. Contact Fidelity for a prospectus, an offering circular, or, if available, a summary prospectus containing this information. Read it carefully.

The Fidelity screeners are research tools provided to help self-directed investors evaluate these types of securities. The criteria and inputs entered are at the sole discretion of the user, and all screens or strategies with preselected criteria (including expert ones) are solely for the convenience of the user. Expert screeners are provided by independent companies not affiliated with Fidelity. Information supplied or obtained from these screeners is for informational purposes only and should not be considered investment advice or guidance, an offer of or a solicitation of an offer to buy or sell securities, or a recommendation or endorsement by Fidelity of any security or investment strategy. Fidelity does not endorse or adopt any particular investment strategy or approach to screening or evaluating stocks, preferred securities, exchange-traded products, or closed-end funds. Fidelity makes no guarantees that information supplied is accurate, complete, or timely, and does not provide any warranties regarding results obtained from its use. Determine which securities are right for you based on your investment objectives, risk tolerance, financial situation, and other individual factors, and reevaluate them on a periodic basis.

The views expressed are as of the date indicated and may change based on market or other conditions. Unless otherwise noted, the opinions provided are those of the speaker or author, as applicable, and not necessarily those of Fidelity Investments. The third-party contributors are not employed by Fidelity but are compensated for their services.

This information is intended to be educational and is not tailored to the investment needs of any specific investor. As with all your investments through Fidelity, you must make your own determination whether an investment in any particular security or securities is consistent with your investment objectives, risk tolerance, financial situation, and evaluation of the security. Fidelity is not recommending or endorsing this investment by making it available to its customers.

Past performance is no guarantee of future results.

The Bloomberg Barclays US Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, US dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, mortgage-back securities (agency fixed-rate pass-throughs), asset-backed securities and collateralised mortgage-backed securities (agency and non-agency).

The S&P 500® Index is a market capitalization-weighted index of 500 common stocks chosen for market size, liquidity, and industry group representation to represent US equity performance.

In general, the bond market is volatile, and fixed income securities carry interest rate risk. (As interest rates rise, bond prices usually fall, and vice versa. This effect is usually more pronounced for longer-term securities.) Fixed income securities also carry inflation risk, liquidity risk, call risk, and credit and default risks for both issuers and counterparties. Unlike individual bonds, most bond funds do not have a maturity date, so holding them until maturity to avoid losses caused by price volatility is not possible. Any fixed income security sold or redeemed prior to maturity may be subject to loss.

High-yield/non-investment-grade bonds involve greater price volatility and risk of default than investment-grade bonds.

Lower yields - Treasury securities typically pay less interest than other securities in exchange for lower default or credit risk.

Interest rate risk - Treasuries are susceptible to fluctuations in interest rates, with the degree of volatility increasing with the amount of time until maturity. As rates rise, prices will typically decline.

Call risk - Some Treasury securities carry call provisions that allow the bonds to be retired prior to stated maturity. This typically occurs when rates fall.

Inflation risk - With relatively low yields, income produced by Treasuries may be lower than the rate of inflation. This does not apply to TIPS, which are inflation protected.

Credit or default risk - Investors need to be aware that all bonds have the risk of default. Investors should monitor current events, as well as the ratio of national debt to gross domestic product, Treasury yields, credit ratings, and the weaknesses of the dollar for signs that default risk may be rising.

Credit and default risk - While MBS backed by GNMA carry negligible risk of default, there is some default risk for MBS issued by FHLMC and FNMA and an even higher risk of default for securities not backed by any of these agencies, although pooling mortgages helps mitigate some of that risk. Investors considering mortgage-backed securities, particularly those not backed by one of these entities, should carefully examine the characteristics of the underlying mortgage pool (e.g. terms of the mortgages, underwriting standards, etc.). Credit risk of the issuer itself may also be a factor, depending on the legal structure and entity that retains ownership of the underlying mortgages.

Interest rate risk - In general, bond prices in the secondary market rise when interest rates fall and vice versa. However, because of prepayment and extension risk , the secondary market price of a mortgage-backed security, particularly a CMO, will sometimes rise less than a typical bond when interest rates decline, but may drop more when interest rates rise. Thus, there may be greater interest rate risk with these securities than with other bonds.

Prepayment risk - This is the risk that homeowners will make higher-than-required monthly mortgage payments or pay their mortgages off altogether by refinancing, a risk that increases when interest rates are falling. As these prepayments occur, the amount of principal retained in the bond declines faster than originally projected, shortening the average life of the bond by returning principal prematurely to the bondholder. Because this usually happens when interest rates are low, the reinvestment opportunities can be less attractive. Prepayment risk can be reduced when the investment pools larger numbers of mortgages, since each mortgage prepayment would have a reduced effect on the total pool. Prepayment risk is highly likely in the case of MBS and consequently cash flows can be estimated but are subject to change. Given that, the quoted yield is also an estimate. In the case of CMOs, when prepayments occur more frequently than expected, the average life of a security is shorter than originally estimated. While some CMO tranches are specifically designed to minimize the effects of variable prepayment rates, the average life is always at best, an estimate, contingent on how closely the actual prepayment speeds of the underlying mortgage loans match the assumption.

Extension risk - This is the risk that homeowners will decide not to make prepayments on their mortgages to the extent initially expected. This usually occurs when interest rates are rising, which gives homeowners little incentive to refinance their fixed-rate mortgages. This may result in a security that locks up assets for longer than anticipated and delivers a lower than expected coupon, because the amount of principal repayment is reduced. Thus, in a period of rising market interest rates, the price declines of MBS would be accentuated due to the declining coupon.

Liquidity - Depending on the issue, the secondary market for MBS are generally liquid, with active trading by dealers and investors. Characteristics and risks of a particular security, such as the presence or lack of GSE backing, may affect its liquidity relative to other mortgage-backed securities. CMOs can be less liquid than other mortgage-backed securities due to the unique characteristics of each tranche. Before purchasing a CMO, investors should possess a high level of expertise to understand the implications of tranche-specification. In addition, investors may receive more or less than the original investment upon selling a CMO.

Investments in mortgage securities are subject to prepayment risk, which can limit the potential for gain during a declining interest rate environment and increase the potential for loss in a rising interest rate environment.

You could lose money by investing in a money market fund. An investment in a money market fund is not a bank account and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. Before investing, always read a money market fund’s prospectus for policies specific to that fund.

Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss. Your ability to sell a CD on the secondary market is subject to market conditions. If your CD has a step rate, the interest rate of your CD may be higher or lower than prevailing market rates. The initial rate on a step rate CD is not the yield to maturity. If your CD has a call provision, which many step rate CDs do, please be aware the decision to call the CD is at the issuer's sole discretion. Also, if the issuer calls the CD, you may be confronted with a less favorable interest rate at which to reinvest your funds. Fidelity makes no judgment as to the credit worthiness of the issuing institution.

Indexes are unmanaged. It is not possible to invest directly in an index.

The Fixed Income Analysis tool is designed for educational purposes only and you should not rely on it as the primary basis for your investment, financial or tax planning decisions.

Diversification and asset allocation do not ensure a profit or guarantee against loss.

Keep in mind that investing involves risk. The value of your investment will fluctuate over time, and you may gain or lose money.

Fidelity Investments® provides investment products through Fidelity Distributors Company LLC; clearing, custody, or other brokerage services through National Financial Services LLC or Fidelity Brokerage Services LLC; and institutional advisory services through Fidelity Institutional Wealth Adviser LLC.